When is enough, enough?

What is the tipping point in used prices?

The used day supply is up everywhere right now. That can be concerning to dealers and is mainly due to retail sales slowing at the end of 2021. The December 2021 U.S. retail auto sales declined 17.4% compared with December 2020. So top of mind for dealers is setting the right strategy going into the new year after coming off such a slow December. The questions that keep getting asked over and over are the following: Should we sell down our inventory? Will the retail demand pick up in Q1? Will used vehicle values keep dropping? Am I getting deeper and deeper underwater? How long will buyers tolerant these high prices? These questions are best answered at the dealership level by working with your marketing and inventory management teams. However, I will attempt to address the root of these concerns below from a Macroeconomic level.

To answer these questions, we first must understand what the industry insiders expect in the next two selling quarters. Speaking to Cox Automotive's Chief Economist Jonathan Smoke, he states, referring to the new Covid variant, "That could make January a bit softer as we are seeing economic activity and sentiment impacted in the most recent data. However, I think the vehicle market will bounce back quickly as tax refund season begins in February. This Omicron wave is expected to peak next week and then decline almost as fast as it surged. With that risk declining, coupled with tax refunds being issued, vehicle demand should be very strong this spring." In addition, we both agree that consumers, hedging against the higher cost of borrowing expected in the second half of the year, could accelerate demand by pulling larger purchases forward. The fed has signaled on a few occasions that we should expect rate hikes starting mid-year. You can read more about the interest rate forecasts HERE.

With market demand expected to strengthen in February, there may be an opportunity to take advantage of the current softness over the next couple of weeks. Working with your inventory management teams, you may be able to flip older higher mileage inventory for newer inventory in preparation for the demand surge. Most dealers are being very cautious not to sell off aged inventory only to decrease day supply. The reason for that caution, as we learned last year, is when the sales rate begins to increase we would likely have to "panic buy" in a market back on the rise to fill our lots and meet the demand. That type of scenario has been shown to erode profits.

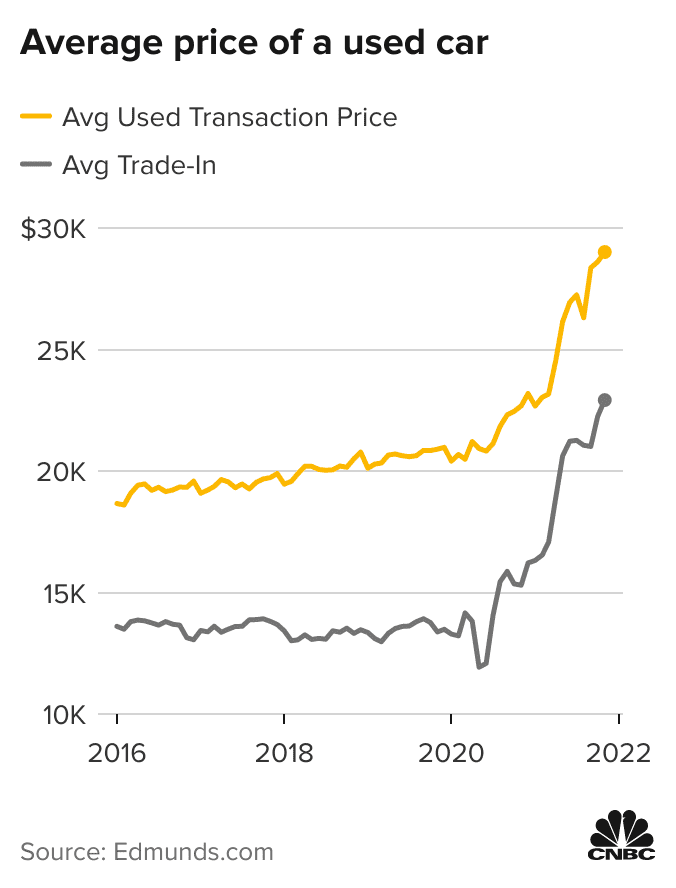

In light of that guidance, the next biggest question I get is around tolerance. When will consumers lose their tolerance to pay these inflated use car prices? To answer that question we have to look at the whole car deal and not just the cost of the vehicle being sold. Looking at the whole deal, we see that both sides of the deal are inflated in most cases, as represented in the graph below. That being the case, the consumer with a trade is not impacted by the inflated used prices as much as it would seem. The equity difference between what they get for their trade and what they pay for the vehicle they purchase is roughly the same or, as shown below, better than it has been historically. Looking at the entire deal structure and not just the cost of the vehicle will help sell more cars and create a more satisfied customer.

The good news is the 2022 forecast from our industry experts is favorable to retail automotive. Demand will increase in the 1st half of the year, and we need to have the day supply on hand to meet that demand. Consumers are still in purchase mode for many reasons. With the valuations still staying strong, the deal today is still the best deal the buyer can get.