EV Battery Recycling

When will it make an impact on battery manufacturing?

In an article by Hans Melin of Circular Energy Storage recapping the Battery Show this week, it seems the theme was recycle, recycle and recycle. The supply chain of minerals is finite and hard to unearth as we all know. However, we are doing it today, and batteries are being produced. Our hope is that we get to a point where we will not have to mine any longer and all the aging batteries in use will be recycled and used to make new batteries in the future. Why would they? According to the industry, 98% of the material can be recycled, and 92% of the minerals can be recovered to make new batteries. That is a very promising outlook; however, it will take time to get there, and we cannont rely on recycling alone to solve our volume needs in the next decade. The indsutry’s outlook is there will come a time when it will be our main or possibly only source. Until then, we will have a supply issue for certain.

Second-life repurposing of those batteries keeps them out of the recycling ecosystem for another few years. That's good for our battery energy storage systems and public infrastructure builds. That suggests that seven to nine year old EVs will be feeding the repurpose industry in the next six to eight years and then move into the recycling stage of lifecycle management after their useful life there. There are roughly 2 million EVs in VIO in North America, and most of them are less than six years old. Using the assumptions above, that put those batteries in the recycle stage of battery lifecycle management in 13 years or 2035. It may take as long as 2050 before we’ll see a significant volume to refill the manufacturing supply chain with recycled minerals. That doesn’t mean it’s not coming. It just means the projections are off, and new minerals in battery manufacturing will be the key to growth for some time.

As mentioned, repurposing batteries will likely be the key supply source for battery energy storage systems over the next 15 or 20 years. With that in mind, it is likely we see the same paradigm we see in the new and used car automotive market today. Battery manufacturers will be feeding market share first. So, just like we have saw with rental car companies for automakers, secondary storage companies may not have the same priority as the consumer segments. That signals BSS, Charing infrastructure companies, and the like should prepare to rely on repurposed batteries to feed their production needs. That dynamic could drive up the cost of repurposed used batteries, just like the supply shortage recently drove up the cost of used cars.

That scenario could force the repurposed asset market to be inflated and a valuable pathway for revenue growth for years to come. At least until we have more capacity in the supply chain of new batteries from recycling. It’s clear to see that the recycling of minerals is one of our best chances at an eco-friendly closed loop system, but it will take time. Says Erik Milen of Circular Energy Storage

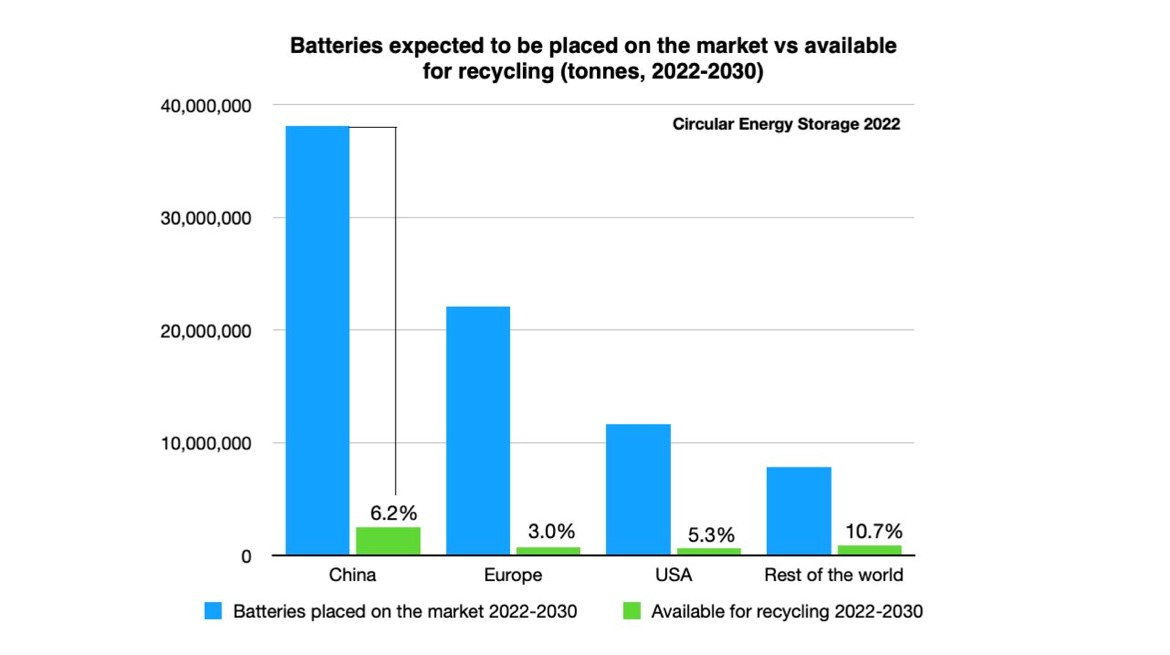

Below is a chart showing Circular Energy Storage's forecast of how many end-of-life batteries will be available for recycling in the next nine years compared to how much we expect to be placed on the market (3.4 TWh in 2030).

Hans makes a valid point in his article that it is almost ironic to see that the market who controls the vast majority of all resources, China, also is the market where we see most initiatives for alternative solutions such as battery swapping, fast charging with smaller batteries, and not least, smaller vehicles.

Is that signal for us all? You can read more from CES’s paper HERE.

Happy Driving, John Ellis CBC

The EV Guy!