Automotive Market Update

Indicators of what's ahead for the remainder 2022 in automotive?

There are many things that can get in our way when running our retail operations day to day. Dealer need a narrow and wide vision to be successful. Dealer’s job is to run their business day to day, week to week and month to month. Retail profits matter but so does the future.

My goal is to reveal the economic indicators driven by external forces but are what consumers and producers can’t control and are the big hurdles we need to overcome. Here are just a few outlined below with my suggested guidance.

How will aging day supply this impact automotive retail. Expect vehicles to keep aging with cars staying in the driveway longer. Fixed operations and F&I should grow significantly in the coming years because of the age of vehicle purchases needing warranties and service contracts along with the average age in VIO growing requiring more service visits to keep on the road.

1. New allocation is back down after a few high weeks, most likely because of the news we saw in the prior week’s regarding production pullback

2. The post sweet spot’s age is growing 13+ model years and is much riskier to recon and get frontline ready due to their age and low vehicle value.

3. The good news is we continue to have high volumes in the aftermarket sweet spot in the 6-12 year old range.

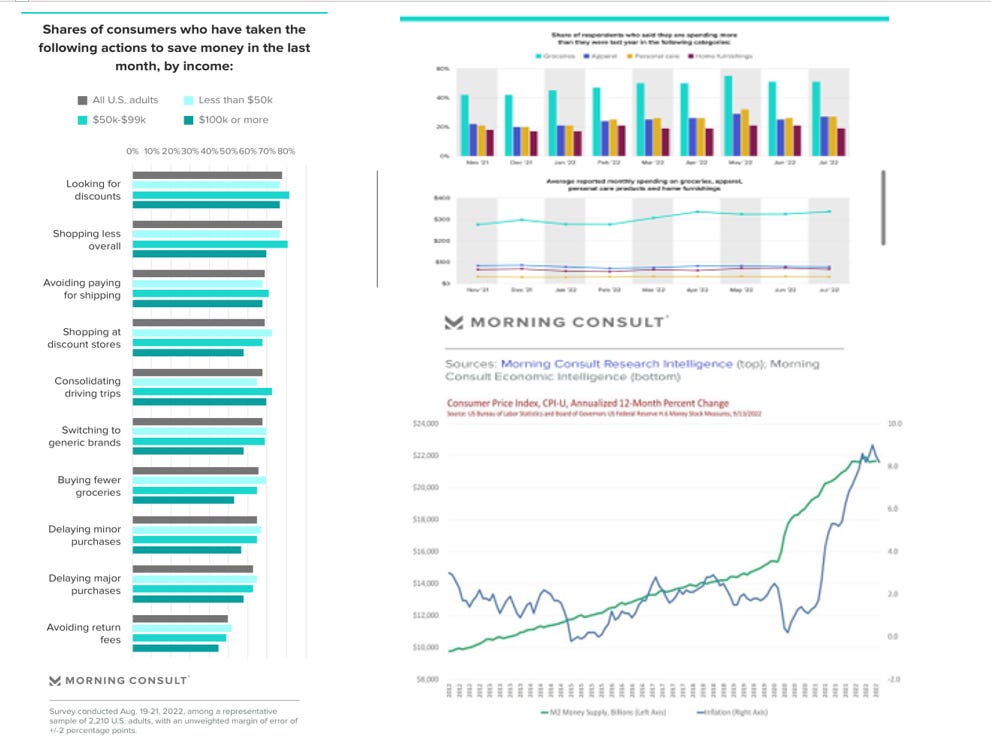

4. Morning Consult report this week inflation is starting to impact the behavior of higher income households as well. It's not surprising to see groceries and food items being the highest overall household expense increase followed closely by apparel and personal care.

5. This data suggests higher income households are starting to become more frugal as well although likely by choice rather than necessity.

6. Consumer price index relative to the M2 money supply. Digging deeper looking into the numbers reveal it’s more about long-term investments and fixed rate termed deposits than the shrinking of liquid cash as M1 seems to be staying steady.

7. CNBC reported this morning that mortgage rates just hit 6%.

All this suggests consumer still have money due to wage growth but the amount of money they’re saving after monthly expenses is diminishing. That will have long-term consequences on the economy if we don’t get it turned around. That is evidence in Experian’s State of the Automotive Finance Market Report: Q2 2022, leasing declined from 27.82% to 19.65% year-over-year, marking the lowest drop in quite some time. Used car prices will continue to stay high with the current outlook in new car availability. The bottoms not falling out just yet. Stay the course, stick to the fundamentals and take market share.

Happy Selling,

John Ellis, CBC

Automotive Consultant

Thanks John!!