Automotive Dealer's Weekly Update 8-25-2022

The Automotive Advisor Team

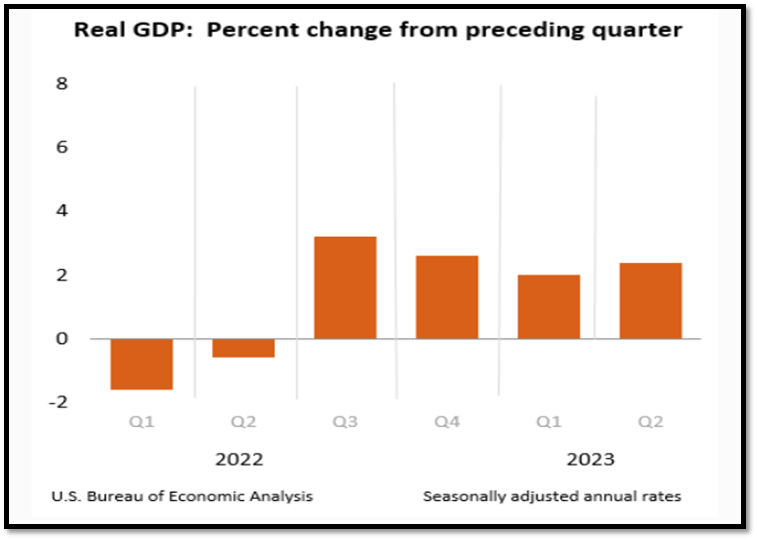

Economic Update:

Q2 2023 real GDP growth came in much stronger than expected and monthly Personal Consumption Expenditure growth reaccelerated in June. Additionally, the consumer confidence index saw meaningful improvement in both June and July. As confirmed again by the recent data, the likelihood of a ‘soft landing’ for the economy is rising, but we continue to believe that a very short and shallow recession is the more likely scenario.

Looking into 2024, the volatility that dominated the US economy over the pandemic period is expected to diminish. In the second half of 2024, Cox Automotive forecasts that overall growth will return to more stable pre-pandemic rates, inflation will drift closer to 2 percent, and the Fed will lower rates to near 4 percent. However, due to an aging labor force, we expect tightness in the labor market to remain an ongoing challenge for the foreseeable future.

All that means, is consumers are still fighting, there is a light at the end of the tunnel for our economy if we stay on the same pace, and rates and inflation will both move in positive directions in a very competitive job market. All good news for retailers.

Read the entire Auto Market Report here: https://theautomotiveadvisorteam.com/740-2/